Two agents chase the same 40-truck fleet. The first sends a submission the day the application comes back. The second runs a carrier analysis first, spots an out-of-service spike from last winter, gets the story from the owner, and puts the explanation in the cover note. Same risk, same market. The second agent gets the quote back in days, not weeks, and binds it.

Carrier analysis is not an underwriter-only skill. The data behind it is mostly public, and the agents growing their commercial trucking book fastest treat it as a standard step between "interested prospect" and "submitted risk." This guide covers what a carrier analysis includes, where the data lives, and the 5-step review to run before you quote.

What Is Carrier Analysis?

Carrier analysis is the review of a motor carrier's public safety and registration data before quoting or writing the risk: authority status, roadside inspections, violations, crash history, fleet size, and insurance filing history. Underwriters run it on every submission. Agents who run it first place more accounts and waste less time on unplaceable ones.

The insurance industry has productized this for decades. Underwriters subscribe to scored dossiers like the CAB report, and Carrier Software sells a similar underwriting snapshot. But the raw material in all of them is largely the same federal data, and that data does not care who is looking at it.

Where Carrier Analysis Data Comes From

Four government sources feed nearly every carrier review:

- The FMCSA census. Every active carrier's identity, address, fleet size, and cargo types, self-reported on the MCS-150 form and updated at least every two years.

- SAFER. The FMCSA's Safety and Fitness Electronic Records system: authority status, safety rating, and inspection and crash summaries by DOT number.

- The Safety Measurement System. The FMCSA's SMS scores carriers across safety categories (unsafe driving, hours of service, vehicle maintenance, and more) on a rolling 24-month window.

- Insurance filings. Liability filings, lapses, and cancellations, which reveal both compliance history and the renewal timing that matters for prospecting.

The catch is fragmentation. Each source answers one question, lives on its own site, and none of them talk to each other. That is the entire reason compiled carrier reports exist: they sell speed, not access.

How to Run a Carrier Analysis in 5 Steps

Run these in order. Each step can disqualify a risk early, and the sequence front-loads the fastest checks.

Confirm the authority

Active operating authority, no unexplained gaps, revocations, or reinstatements. An authority that blinked off and back on has a story, and the underwriter will want it. A carrier running under a brand-new DOT number with a familiar address deserves a harder look.

Read 24 months of inspections

Inspection count, violation types, and out-of-service events over the rolling two-year window. One bad inspection is noise. A pattern of maintenance violations or driver OOS events is the number one reason a submission stalls in underwriting.

Pull the crash history

Reportable crashes with dates, severity, and whether they cluster. Crashes are not automatically disqualifying, but an unexplained crash the applicant did not mention is. Get the narrative from the carrier before the underwriter asks for it.

Square the equipment

Compare the fleet size on the application against the distinct vehicles showing up in roadside inspections. The application says 5 power units but 9 VINs were inspected last year? That gap means trip leasing, unreported equipment, or shared iron, and every one changes the risk.

Check insurance history and renewal timing

Filing lapses and cancellations flag a carrier that struggles to stay covered. The expiration date tells you when the account is actually winnable. A clean carrier 45 days from renewal is worth more of your week than a spotless one that just bound elsewhere.

The Pre-Quote Carrier Analysis Checklist

- Authority: active, no unexplained gaps or revocations

- Inspections: 24 months reviewed, OOS patterns explained

- Crashes: history pulled, narratives gathered from the carrier

- Equipment: inspected VIN count squares with the application

- Insurance: no filing lapses, renewal window confirmed

Carrier Analysis Works Offense, Not Just Defense

Most agents meet carrier analysis as a defensive move: avoid the decline, tighten the submission. The bigger payoff is on offense, deciding which carriers to pursue in the first place.

Run the same analysis across a list instead of a single prospect and it becomes a ranking engine. Start from a filtered set of DOT leads in your states, screen out the carriers whose safety profile no market will touch, and sort the rest by insurance renewal date. The result is a call list where every name is placeable and timely, before you have dialed anyone. That is the difference between prospecting from raw census data and prospecting from analyzed data.

It also compounds in referrals and renewals. An agent who walks into a fleet conversation already knowing the carrier's inspection profile and equipment mix reads as a specialist, because that is what specialists do.

Running the Analysis in One Click

Everything above can be done by hand across SAFER, SMS, and the filing databases in 15 to 30 minutes per carrier. That is fine for one submission and unworkable for a pipeline.

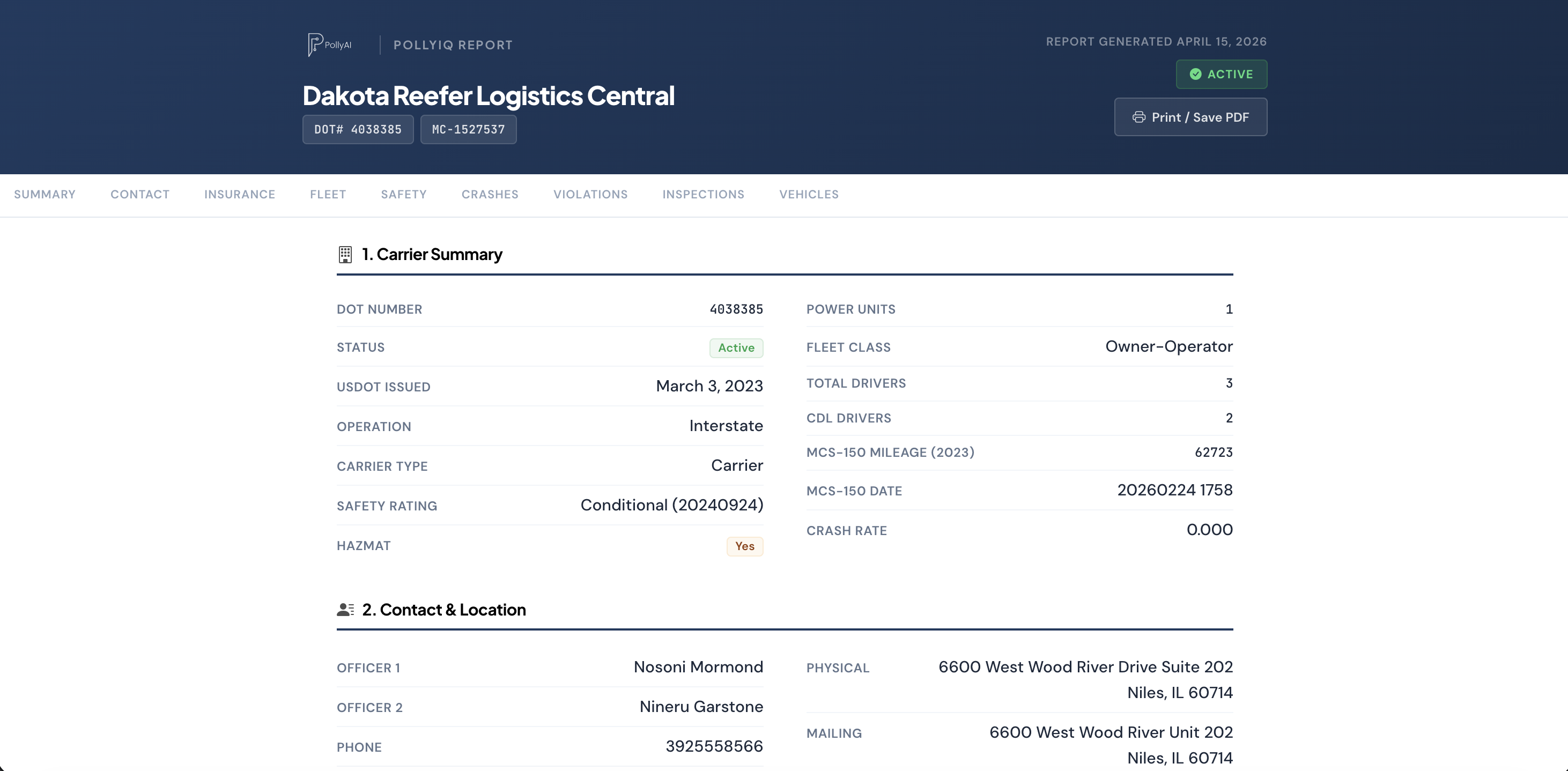

PollyAI compiles the full workup automatically. The PollyIQ carrier report puts authority status, safety scores, 24 months of roadside activity, crash history, inspection citations, and VIN-level equipment on one print-ready page for any DOT number. Pre-underwrite a prospect before the first call, or attach the report to the submission so the underwriter's own carrier analysis confirms what you already told them. It is included with every PollyAI plan, starting at $39 per month.

Carrier Analysis FAQs

What is carrier analysis in trucking insurance?

It is the review of a motor carrier's public safety and registration data before quoting: authority, inspections, violations, crashes, fleet size, and insurance history. Underwriters run it on every submission; the best agents run it first.

Is the data used in a carrier analysis free?

Mostly, yes. Authority, safety, inspection, crash, and filing data are public FMCSA records. The cost is time, because the data is spread across separate government systems. Compiled reports sell speed, not access.

What is the difference between a carrier analysis and a CAB report?

A CAB report is the subscription product underwriters use for carrier analysis, with Central Analysis Bureau's proprietary scoring layered on public data. The analysis itself can be run on the same public facts without a subscription.

How long does a carrier analysis take?

Manually, 15 to 30 minutes per carrier across SAFER, SMS, and the filing systems. With a compiled report, about a minute.